|

|

|

Glossary - SFOpenBook Spending & Revenue

Table of Contents

Tabs:

Filters:

Data Table:

Other Terms

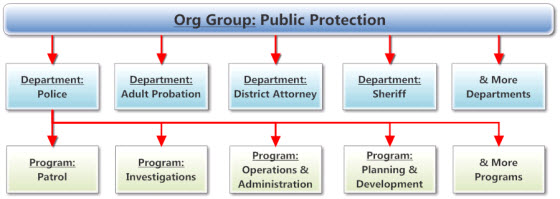

Organization TabThis tab shows three levels of detail (Org Group, Department and Program) that classify activity by organizational unit. Each Org Group consists of one or more Departments, and each Department consists of several Programs. The chart below shows the hierarchy of the Organization tab through the example of the Org Group Public Protection and the Police Department.

Organization Group - In the Organization tab, Org Group is the highest level of detail, and generally represents a group of Departments. For example, the Public Protection Org Group includes Departments such as the Police Department, Adult Probation, the District Attorney, and the Sheriff.

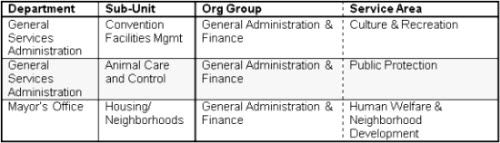

Note that Org Groups are similar to - but in a few cases different than - Major Service Areas (MSAs) that are used in the City and County’s year-end financial statements (Consolidated Annual Financial Report, or CAFR). As shown in the table below, sub-units of two departments are reported in different Major Service Areas, but belong to one Organization Group.

Department - In the Organization tab, Department is the middle level of detail. Departments are the primary organizational unit used by the City and County of San Francisco. Examples of Departments are Recreation and Parks, Public Works, and the Police Department. See the Department List for a complete list of departments.

Program - In the Organization tab, Program is the lowest level of detail. A program identifies the services departments provide. For example, the Police Department has programs for Patrol, Investigations, and Administration.

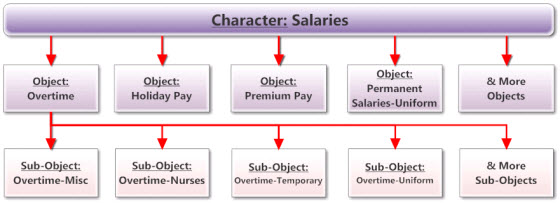

Type TabThis tab shows three levels of detail (Character, Object and Sub-object) that group spending and revenue activity by type. For example, spending on office supplies throughout the City is identified using a sub-object. Each Character consists of several Objects, and each Object consists of several Sub-Objects. The chart below shows the hierarchy of the Type tab through the example of the Salaries Character and the Overtime Object.

Character - In the Type tab, Character is the highest level of detail for type of activity. For example, salaries, benefits, contractual services, and materials & supplies are recorded as different Characters.

Object - In the Type tab, Object is the middle level of detail for type of activity. For example, within the Salaries Character, Objects differentiate between Permanent Salaries, Temporary Salaries, and Overtime pay.

Sub-object - In the Type tab, Sub-object is the lowest level of detail for type of activity. For instance, within the Overtime Object, Sub-object segregates overtime for nurses from overtime for police officers and fire fighters (known as uniformed staff).

Sub-objects are the lowest level of Type data available in SFOpenBook Spending and Revenue. For instance, under the Equipment Purchases Object, there is no additional information on the Automotive & Other Vehicles Sub-object, so you will not be able to identify what cars were purchased and for what amount. However, you can use Vendor Payment Summaries to get detail by vendor and document.

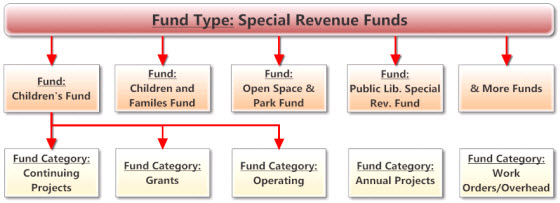

Fund TabThis tab shows three levels of detail (Fund Type, Fund, and Fund Category) for how the City segregates pots of money for particular uses into fund accounts. For instance, the General Fund is used for many purposes, while Pension Trust Funds are used only to administer benefits to retirees. The use of funds is governed by law and/or accounting standards.

Fund Type - In the Fund tab, Fund Type is the highest level of detail for fund accounts, and is used to group Funds according to governmental accounting standards.

Fund - In the Fund tab, Fund is the middle level of detail for fund accounts. For example, within the Special Revenue Fund Type, you can find the Children’s Fund and the Open Space & Park Fund.

Fund Category - In the Fund tab, Fund Category is the lowest level of detail for fund accounts. Within Fund, Fund Categories group activity by their characteristics: Operating, Annual Projects, Continuing Projects, Grants, Interdepartmental/Work Order.

A note about the annual and continuing fund categories: Unspent money that was budgeted for annual projects is returned to fund balance at the end of the fiscal year; those funds must be appropriated (budgeted) in the following year before they can be used. Unspent money budgeted for continuing projects remains dedicated and available for the original purpose across fiscal years.

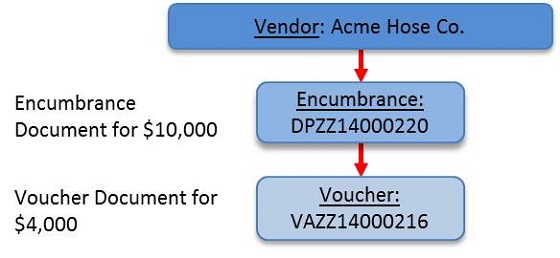

Vendor TabUse the Vendor tab to view activity by vendor, and then optionally drill to encumbrance and voucher document detail.

Here is an Example of the process for paying vendors explaining the columns shown on the vendor tab:

- Assume the Fire Department is buying $10,000 worth of fire hoses from the Acme Hose Company in two groups. First an encumbrance document would be created for $10,000; at this point the remaining balance column would show $10,000.

- The vendor, Acme Hose Company, delivers $4,000 worth of hoses, so the Fire Department requests a payment of $4,000 against the encumbrance by creating a voucher document. Now the remaining balance would be $6,000 and "Pending Amount" would show $4,000.

- A few days later, the check or electronic payment is issued to the vendor. The remaining balance is still $6,000, but "Pending Amount" becomes zero and "YTD Payments" shows $4,000.

Vendor - An organization that the City pays in return for goods or services.

Encumbrance - An Encumbrance is a document that reserves a specific amount of money for payment to a vendor for a specific purpose. Purchase Order is another commonly used name for this.

Voucher - A Voucher is a request for payment. This can either be a payment using funding reserved in an Encumbrance, or it can be a Direct Payment.

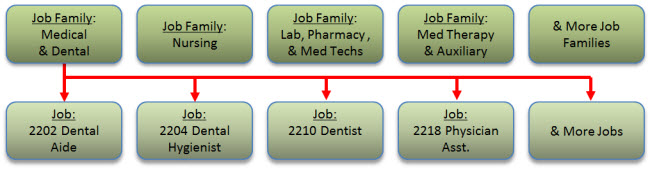

Job - This tab shows two levels of detail (Job Family and Job) when the report type Staffing (FTE) is selected.

Job Family - In the Job tab, Job Family is the highest

level of detail and is used to combine similar Jobs into meaningful groups.

Job - In the Job tab, Job is the

lowest level of detail. Within Job Family, Jobs are defined by the Human Resources classification unit. Examples include gardeners, police officers, and accountants.

Fiscal Year (FY) - An accounting period of 12 months. The City and County of San Francisco operates on a fiscal year that begins on July 1 and ends on June 30 the following year. The Fiscal Year ending June 30, 2012 is represented as FY2011-2012.

Revenue - Money received in the current fiscal year or reserved from a prior year. For example, when the City receives money from taxes, this is revenue. The strict accounting definition of this money would be "Sources."

Spending - Money spent in the current period or reserved for use in a future period. For example, when the City buys office supplies, this is spending. The strict accounting definition of this money would be "Uses."

Vendor Payments - Payments made to vendors. This includes for-profit and non-profit organizations and is a subset of all spending. See the glossary entry for Vendor Tab for an example describing the vendor payment process.

Non-Profit Vendor - Financial activity with vendors that are non-profit organizations as defined through the City's business tax process.

Staffing (FTE) -

Staffing level is represented by "Full Time Equivalent (FTE)". One FTE equals one or more employees

who together work 40 hours per week. For instance, an employee who

works 40 hours per week is counted as one FTE,

and two part-time employees who each work 20 hours per week are

also counted as one FTE. Overtime hours are excluded from this calculation. FTE is relative to the time period.

Annual FTEs are based on 2080 hours per year. FTE is calculated by dividing hours worked by the normal hours per year,

and totals may not sum due to rounding.

Related Gov't Units - In SFOpenBook, these are fiduciary funds and component units that are included in the City’s financial statements but are different in nature from the other funds and organizations in City government. Fiduciary Funds include all Trust and Agency Funds that account for assets held by the City as a trustee or as an agency for individuals or other governmental units. Pension Trust funds are one example of a fiduciary fund, where the government holds pension savings in trust for employees. Component units are legally separate entities that have significant financial and operational relationships with the City. The specific funds affected by the Related Gov't Units filter are shown below.

- Fiduciary Funds

- Agency (7A)

- Successor Agency-Former SF Redev Agency (7S)

- Pension Trust (7P)

- Other Employee Benefit Trust (7Q)

- Retiree Health Care Trust (7R)

- Component Units

- SF Redevelopment Agency (8R)

- Treasure Island Development Authority (8A)

Transfer Adjustments - Amounts that eliminate double counting of activity that is recorded twice in the City’s accounting system.

Transfer Adjustments (Basic Explanation)

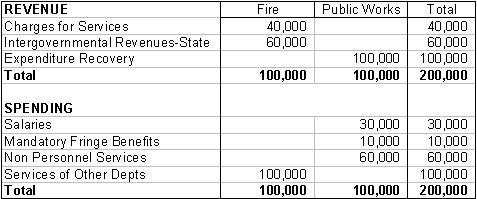

To meet accounting needs, money can be moved from one fund or department to another. For example, Public Works provides building maintenance services for the Fire Department for which the Fire Department pays Public Works.

-

Fire gets a variety of revenue, some of which it spends for Services of Other Depts

-

Public Works gets revenue in the Expenditure Recovery Character which it spends on Salaries, Benefits and Contractual Services to provide the building maintenance services

-

The table below shows that the $100,000 of spending & revenue for this activity would be double counted when looking at total City and County spending & revenue.

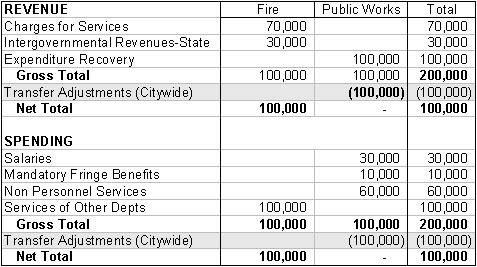

To solve this double counting problem, SFOpenBook shows a reduction of $100,000 called Transfer Adjustments (Citywide) to the spending & revenue for the department providing the service. This lets us display both the gross total of activity for both departments and the net total use of City and County revenues.

Transfer Adjustments (Citywide)

In the example above, the money is moving both between departments, from Fire to Public Works, and between funds, from General Fund Operating to General Fund Works Orders/Overhead.

- Transfer Adjustments (Citywide) are used when money is moved from one department to another. These are deducted from the gross total to create the net total.

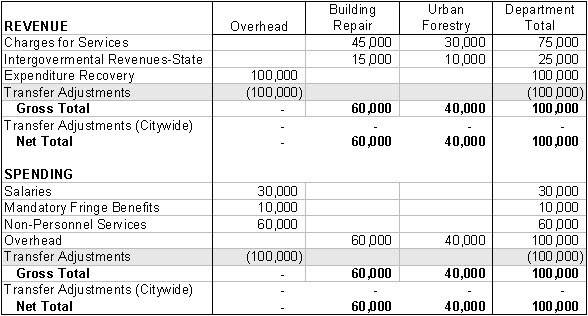

- Transfer Adjustments are included in the gross total when they are within the same department. A separate sub-object is used to distinguish departmental Transfer Adjustments from Transfer Adjustments (Citywide).

Transfer Adjustments (within the same department)

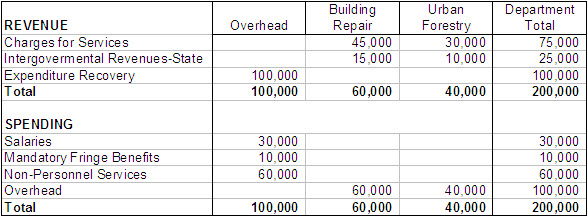

An example of a Transfer Adjustment within a department would be Public Works overhead allocations. Overhead costs cannot easily be isolated to a direct service or unit and so are allocated across those units using accepted accounting methods. Central management costs are allocated to the different parts of Public Works (e.g. Building Repair, Urban Forestry, Construction Management).

$100,000 of activity is double counted within the department.

In this case, the Transfer Adjustments are shown in the Gross Total since the double counting is within one department.

Transfer Adjustments (for Revenue Transfers)

The examples above involved Expenditure Recovery; the other kind of activity that requires Transfer Adjustments involves Revenue Transfers.

-

Revenue Transfers move revenue from one fund to another as required by governmental accounting standards.

-

Transfer Adjustments for Revenue Transfers work much like those for Expenditure Recovery.

-

They are recorded with a Revenue Transfer Out and a Revenue Transfer In Character (in the Type hierarchy) instead of using Services of Other Departments and Expenditure Recovery.

-

They can be within the same department or they can be between different departments.

-

The Transfer Adjustment is shown in the fund with the Revenue Transfer Out as shown in the following example of a transfer from Fund A to Fund B.

Gross Total - The total amount of spending or revenue, including some activity that is double counted because it is recorded in two departments to support departmental accounting needs. See Transfer Adjustments for a more detailed explanation of this.

Net Total - The total after Transfer Adjustments (Citywide) is removed from the Gross Total to eliminate double counting when money is moved from one department to another. See Transfer Adjustments for a more detailed explanation of this.

Pending Amount - The payments that have been requested but not yet paid. See the definition of Vendor Payments for an example explaining this in more detail. If looking at a 5-year period, this is the payments requested but not yet paid as of the most recent year shown.

Direct Payment - A payment where there is no encumbrance.

No Vendor - Spending that is not related to a vendor or which represents accounting adjustments.

Remaining Balance - The unused portion of an encumbrance document. See the definition of vendor payments for an example. If looking at a 5-year period, this is the remaining balance as of the most recent year shown.

Work Order - Money one department pays to another department for services received. For example, the San Francisco Public Utilities Commission (PUC) pays the Department of Public Works for construction services on new sewer lines using a Work Order. Work Orders can be identified in the Type hierarchy; they use the Services of Other Departments Spending Character and the Expenditure Recovery Revenue Character.

Transfer (Revenue Transfer) - Money transferred from one fund to another. This is recorded using a Revenue Transfer Out Spending Character and a Revenue Transfer In Revenue Character (in the Type hierarchy). Revenue transfers between funds can be within the same department, or from one department to another.

|

|

|